Product cost vs Procurement teams.

Product cost | May 18, 2022 | By

Across every industry, companies that have a competitive advantage are those that launch well-thought-out and well-designed products in a timely fashion. Moreover, given the market conditions of shrinking product life cycle times and consistent low-cost-high-quality product expectations from consumers, companies are required to introduce new products to the market faster for better ROI. But, the rollout of new products has slowed down in recent years. These are due to the never-ending pandemic, labor and material shortages, and the multi-country geopolitical tussle that has taken the world by storm. And unfortunately, some of these issues are starting to take new forms. Yet, consumer demand is surging, and businesses are working hard to crank up their engines to work against time to cater to the demand.

The successful companies will be those returning to or have stuck to the basics of procurement and supply chain. And companies that concentrate on product costs will be the torchbearers of success. Therefore, as important as it is to provide a highly reliable product, and launch it on time, delivering products at the target cost is a basic requirement and not a choice for companies to succeed.

What is Product Cost?

Product cost is one of the major expenses for any product manufacturing company. It is the cost that makes up for producing the product. It includes direct material, direct labor, consumable production supplies, and factory overheads. Direct material costs eat up a large portion, around 65-80% of the Cost Of Goods Sold (COGS).

Cost of Goods Sold is the total cost of producing or manufacturing all of the goods sold by an organization. It includes the cost of the raw materials or direct materials (materials that directly impact the production of the goods), transportation costs, storage costs, and cost of labor, but not the indirect expenses associated with the sales and distribution of the product. COGS is viewed as an expense and is reported on the company’s income statement. Since it is the cost of doing business, COGS gives the management a good indication of how efficient the company’s commercial activities are or, in other words, knowing the financial stability. These help the stakeholders identify how they can reduce production costs, increase income, and make informed decisions regarding an organization’s future.

Given the sizeable contribution of product cost to COGS, you would think that companies are on top of their product costs. Unfortunately, the situation is not so. Meeting the product cost target before the start of production of the actual product is a complex art akin to predicting the stock market.

There are two ways or strategies that product manufacturing companies use to control product costs: Cost Reduction or Cost Avoidance.

Cost Reduction vs. Cost Avoidance

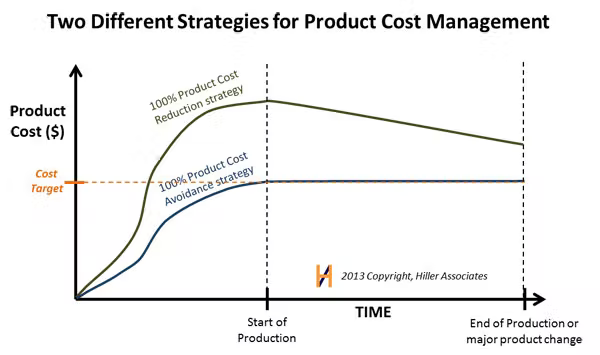

The below graph shows the product cost over time in the product lifecycle. In the cost reduction strategy, companies put little effort toward controlling the product cost during the product development phase. Then, as cost increases due to part revisions or additions, companies exceed the cost target. And, to reduce the cost, companies go through the work of value analysis/engineering, demanding continuous price reduction from the suppliers and other cost reduction methods.

Fig1: Image Source – Hiller Associates.

For example, we know that companies need to continuously launch new products or upgrade existing ones to sustain themselves in the market. And this requires going through the complete cycle of New Product Development every time. Imagine an automotive company working on upgrading its existing model. The upgrade could be anything from providing a facelift to improving the engine power and the like. All of the above changes require changing a component or two in the existing model. After finalizing the design, the procurement and sourcing teams decide on the suppliers to procure the revised parts. And then, the production begins after the plant receives all requisite materials/components. Only now the concerned teams/personnel will initiate the cost reduction strategy through several techniques, such as lean, value analysis, or procurement demanding year-over-year cost reductions.

On the other hand, the cost avoidance strategy is on the opposite side of the spectrum. Here, a large amount of the effort is spent early in the product development process with the involvement of procurement and sourcing teams and suppliers to achieve the product cost target. However, little effort is spent on cost reduction activities after the product launch. One would be inclined to think that most companies would go for cost avoidance. Unfortunately, it’s not so. Many companies focus the majority of their resources on cost reductions after the product’s launch and not before it. This is because cost reduction is easily measurable while cost avoidance is not.

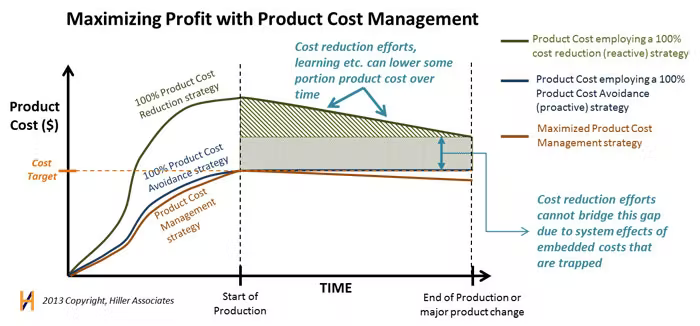

Fig2: Image Source – Hiller Associates.

The above graph shows a two-part split between the cost reduction and the cost avoidance segments. The first triangular area shows that even after years of cost reduction efforts, companies are unable to bridge the gap. The time it takes to reduce costs in this triangular area is known as lost profit. Trying to reduce costs after the start of production means a lot of it must go into trying to reduce them. Also, any cost reduction efforts after the production release will only reach the end of the triangular part. And as per a 2010 Aberdeen study, engineering changes made after a product moves to production cost 75% more than those made before. What is the solution then?

In addition to Cost Reduction, companies should also practice Cost Avoidance, to increase their profits. Despite having robust processes and the right people in the right place, most organizations fail to achieve the cost target. One of the reasons could be the lack of enterprise-wide visibility to drive data- and insight-driven decision making.

But what if there is a single digital platform where all the stakeholders can see how the new product is performing cost-wise and understand how it fits within the cost target during every stage-gate of the NPD process?

What if the platform can automatically roll up all the component cost workings in a single place?

And what if the stakeholders also knew at what stage every component of the BOM is in the procurement lifecycle?

Use Zumen for your Product Cost and Costing Approvals

See, arriving at the target product cost is a team sport. In general, most successful companies go with a team approach to product costing during the NPD process, fostering collaboration among the design engineers, costing engineers, and manufacturing and supply chain management teams. Let us take the World Series 2016 as an example. New York Yankees went all guns blazing to buy the best players in the market, only to see the Chicago Cubs (#14 in player salaries) take home the coveted World Series that year. Irrespective of the sport played, in any team game, however best the players are in their respective positions, the team will not achieve their winning goal in the absence of a cohesive system or process.

Zumen’s Source-to-Contract helps organizations with a purpose-built unified tool that replaces the countless tools organizations use for product cost optimization. Given that one of the primary roles of Procurement and Sourcing teams is to achieve the target product cost, Zumen helps them with the structured data they need to achieve it.

A centralized repository of all communications, negotiation timelines, design revisions, detailed supplier quotations, product price revisions, material cost trends, distribution of raw material sourcing between suppliers, part purchase history and much more are readily available.

Also, Zumen helps purchasers and other stakeholders capture every activity along the cost approval process, by pulling up relevant costs from ERP, roll-up BOM costs from individual part cost estimates, buyer and value analyst estimates, and PO costs.

Schedule a free demo to know more about what Zumen can do to help you.